One of my dividend-growth stocks, Novartis (NVS), increased its annual dividend by 2.3% today, raising the payment from CHF 2.20 to CHF 2.25 per share (CHF = Swiss Franc). This marks the company's 15th consecutive year of dividend growth in CHF.

I will not know the exact amount of the dividend in U.S. dollars (USD) until I receive it. However, with the current exchange rate being 1 CHF = 1.1059 USD, that gives an estimated amount of $2.4884. My understanding is that last year's amount was $2.3527, so the dividend increase in USD would be about 5.8%.

Given that I own 35 shares of NVS, my annual dividend will be about $87.09 before tax or $56.61 after the 35% foreign tax is withheld (which I can claim when I file my U.S. income taxes). I am not a fan of the dividend being paid annually (rather than quarterly) or the foreign tax withholding, but I can live with it. This dividend increase boosts my yield on cost to 4.44%.

Update (April 10): I have now received my NVS dividend. My estimates were pretty close -- it was $86.88 before tax and $56.47 after the 35% foreign tax withholding.

Thursday, February 23, 2012

Tuesday, February 21, 2012

Dividend Increase: GPC

One of my dividend-growth stocks, Genuine Parts Company (GPC), increased its quarterly dividend by 10.0% today, raising the payment from $0.45 to $0.495 per share. This puts the company on track for its 56th consecutive year of dividend growth, which is pretty amazing. Given that I own 50 shares of GPC, my quarterly dividend increases from $22.50 to $24.75, which will add an extra $9.00 to my annual dividend income. This dividend increase also boosts my yield on cost to 3.67%.

Monday, February 20, 2012

Book Review: Sensible Stock Investing

Sensible Stock Investing (2008) by David P. Van Knapp

In this book the author lays out a complete plan for picking, valuing, and managing stocks. The book is divided into six parts (plus two appendices). Part A is an introduction that discusses why stock investing is the best way to build wealth and outlines three steps for becoming a "Sensible Stock Investor." (The three steps are the topics of Parts C-E.) Part B provides a general overview of the stock market and how it works, touching on topics such as market efficiency and bubbles. These first two parts were pretty basic and did not provide much in the way of information that I had not already read elsewhere.

Part C starts to get into the meat of the book by covering how to pick companies in which to invest. The author gives some good advice here; in particular, I like the emphasis on writing a "Story" about a company that summarizes what it does, how it makes money, etc. Part D discusses how to value stocks, providing an overview of valuation in general and a system for scoring stocks on different valuation measures.

Part E covers portfolio management and includes discussion of risk, diversification, types of stocks, momentum, timing, and buy/sell considerations. It is here that I started to get some mixed feelings about the author's strategy because it shifts from an investing strategy to more of a trading strategy with a strong emphasis on setting stop-loss triggers. For example, based on the strategy it can be okay to buy an extremely overvalued ("bubble") stock if it shows favorable price momentum. I thought this part of the book made the strategy less focused. Part F describes two real-life portfolios that were constructed and managed according to the strategy during the 5-year time span that the book was being written. While it was refreshing to see the author put his strategy into action rather than keeping it abstract, the results were okay but not overly supportive.

In summary, I found Parts C and D to be the strongest parts of the book because they provided good discussion of company selection and stock valuation that included a useful scoring system. I found Part E to be the weakest part, although other readers might find more value in some of the portfolio management suggestions. Overall, I think people would do okay if they were to follow the strategy described in this book.

Note: I read this book in February 2012.

In this book the author lays out a complete plan for picking, valuing, and managing stocks. The book is divided into six parts (plus two appendices). Part A is an introduction that discusses why stock investing is the best way to build wealth and outlines three steps for becoming a "Sensible Stock Investor." (The three steps are the topics of Parts C-E.) Part B provides a general overview of the stock market and how it works, touching on topics such as market efficiency and bubbles. These first two parts were pretty basic and did not provide much in the way of information that I had not already read elsewhere.

Part C starts to get into the meat of the book by covering how to pick companies in which to invest. The author gives some good advice here; in particular, I like the emphasis on writing a "Story" about a company that summarizes what it does, how it makes money, etc. Part D discusses how to value stocks, providing an overview of valuation in general and a system for scoring stocks on different valuation measures.

Part E covers portfolio management and includes discussion of risk, diversification, types of stocks, momentum, timing, and buy/sell considerations. It is here that I started to get some mixed feelings about the author's strategy because it shifts from an investing strategy to more of a trading strategy with a strong emphasis on setting stop-loss triggers. For example, based on the strategy it can be okay to buy an extremely overvalued ("bubble") stock if it shows favorable price momentum. I thought this part of the book made the strategy less focused. Part F describes two real-life portfolios that were constructed and managed according to the strategy during the 5-year time span that the book was being written. While it was refreshing to see the author put his strategy into action rather than keeping it abstract, the results were okay but not overly supportive.

In summary, I found Parts C and D to be the strongest parts of the book because they provided good discussion of company selection and stock valuation that included a useful scoring system. I found Part E to be the weakest part, although other readers might find more value in some of the portfolio management suggestions. Overall, I think people would do okay if they were to follow the strategy described in this book.

Note: I read this book in February 2012.

Friday, February 17, 2012

Stock Bought: GIS

Today I bought shares of General Mills (GIS), one of the largest food companies in the world. Its well-known brands include Betty Crocker, Cheerios, Green Giant, Pillsbury, and Yoplait. The company holds the No. 1 or 2 spot for retail sales in many food categories in the U.S. market.

GIS is a good dividend-growth stock. The company (and its predecessor firm) has paid uninterrupted dividends for 113 years and increased its dividend for 8 consecutive years, with a 5-year dividend-growth rate of 11.1%. Incredibly, during those 113 years the company has never reduced its dividend. To me, that is a strong signal that the dividend is a top priority for management.

The stock dipped nearly 4% today after the company lowered its earnings guidance for its fiscal third quarter, citing softer U.S. demand. However, I am not overly concerned by this news. Even if there is a slowdown in earnings growth in the U.S., I foresee much of the future earnings growth coming from overseas, as is the case with many companies that sell consumer staples.

I bought 25 shares of GIS at the price of $38.19 per share, which is less than the price of my existing position, so I was able to average down. I now have a total of 70 shares at an average price of $39.00 per share, giving me a 3.13% yield on cost. At the current dividend rate, I can expect to receive quarterly dividends of $21.35, compared with the $13.73 I was getting before this purchase. GIS will now contribute a total of $85.40 to my annual dividend income.

Incidentally, GIS is one of only two stocks in my portfolio that I am currently able to average down on. The other stock is NSC, but I just added to my position a few weeks ago, so I have decided to hold off on further increasing my position for the time being. However, if it drops even more, then I will likely be compelled to make another purchase.

The market's year-to-date performance has made it increasingly hard to find good deals, but hopefully there will be a pullback in the next few weeks. Market timing is difficult, though, so my plan is to try to make regular monthly purchases and take advantage of whatever opportunities are available at the time. Right now I have enough cash on hand to make one more purchase in February.

GIS is a good dividend-growth stock. The company (and its predecessor firm) has paid uninterrupted dividends for 113 years and increased its dividend for 8 consecutive years, with a 5-year dividend-growth rate of 11.1%. Incredibly, during those 113 years the company has never reduced its dividend. To me, that is a strong signal that the dividend is a top priority for management.

The stock dipped nearly 4% today after the company lowered its earnings guidance for its fiscal third quarter, citing softer U.S. demand. However, I am not overly concerned by this news. Even if there is a slowdown in earnings growth in the U.S., I foresee much of the future earnings growth coming from overseas, as is the case with many companies that sell consumer staples.

I bought 25 shares of GIS at the price of $38.19 per share, which is less than the price of my existing position, so I was able to average down. I now have a total of 70 shares at an average price of $39.00 per share, giving me a 3.13% yield on cost. At the current dividend rate, I can expect to receive quarterly dividends of $21.35, compared with the $13.73 I was getting before this purchase. GIS will now contribute a total of $85.40 to my annual dividend income.

Incidentally, GIS is one of only two stocks in my portfolio that I am currently able to average down on. The other stock is NSC, but I just added to my position a few weeks ago, so I have decided to hold off on further increasing my position for the time being. However, if it drops even more, then I will likely be compelled to make another purchase.

The market's year-to-date performance has made it increasingly hard to find good deals, but hopefully there will be a pullback in the next few weeks. Market timing is difficult, though, so my plan is to try to make regular monthly purchases and take advantage of whatever opportunities are available at the time. Right now I have enough cash on hand to make one more purchase in February.

Dividend Increase: ABT

One of my dividend-growth stocks, Abbott Laboratories (ABT), increased its quarterly dividend by 6.3% today, raising the payment from $0.48 to $0.51 per share. This puts the company on track for its 40th consecutive year of dividend growth before it splits into two companies by the end of this year. Given that I own 45 shares of ABT, my quarterly dividend increases from $21.60 to $22.95, which will add an extra $5.40 to my annual dividend income. This dividend increase also boosts my yield on cost to 3.85%.

Thursday, February 16, 2012

Dividend Increase: KO

One of my dividend-growth stocks, Coca-Cola (KO), increased its quarterly dividend by 8.5% today, raising the payment from $0.47 to $0.51 per share. This puts the company on track for its 50th consecutive year of dividend growth, which is a fantastic streak. Given that I own 30 shares of KO, my quarterly dividend increases from $14.10 to $15.30, which will add an extra $4.80 to my annual dividend income. This dividend increase also boosts my yield on cost over the 3% mark to 3.10%.

Tuesday, February 14, 2012

Personal Finance: Money Flow

A recent article at Seeking Alpha by Tim McAleenan made me think critically about how money flows in my life. The issue addressed in the article was whether investors should always reinvest their dividends or use some of that income for discretionary expenses such as concerts and vacations. In other words, to what degree should dividends be used to build future wealth compared with providing immediate (or near-term) gratification?

In the first part of my comment on the article I wrote:

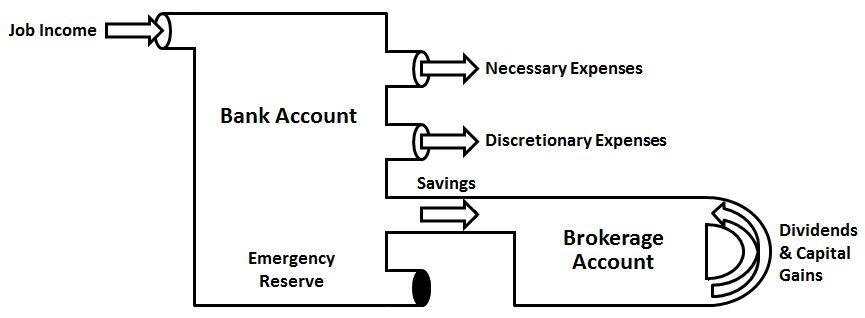

My money resides in two places: my bank account and my brokerage account. My bank account has a single inflow: job income, which is constant from month to month. I need to ensure that I make judicious use of my job income, so it is important to monitor how much of it goes to expenses. The first outflow is money used to pay for necessary expenses, such as rent, utilities, food, etc. It is first because it is essential for my income to cover my basic needs. The second outflow is money used to pay for discretionary expenses, such as concerts, vacations, entertainment, eating out, etc. I have more control over this outflow because I can choose whether I want to spend money on those things (hence the label "discretionary"). If I want immediate gratification, then I can use this money to buy whatever I think will give me it. However, there is a tradeoff: the more money I spend on discretionary expenses, the less money is left over for the third outflow, which is savings for investment. As part of this blog I keep track of my monthly savings.

Savings flow from my bank account into my brokerage account, where I use the money to invest in dividend-growth stocks. An important aspect of my brokerage account is that it has no outflows. Dividends and capital gains from my investments are reinvested, as indicated by the loop in the diagram. As noted on my Strategy page, dividend reinvestment is a key part of my compounding machine for generating a sustainable, rising stream of dividend income. I consider the outflow restriction to be an important aspect of my investing discipline: Money for and from investments is not to be used except for its intended purpose, which is to fund my future retirement. Any money I need to pay current expenses has to come from my bank account.

Of course, circumstances may arise where I suddenly need access to a large sum of money that exceeds my monthly job income. If that happens, then I make use of the Emergency Reserve indicated on the diagram. This is a fair-sized amount of money residing in my bank account that is set aside for emergencies. I can make use of it without having to touch my investments, which again helps to maintain discipline. Notice that its outflow is capped, which means I do not take money out of it unless it is absolutely necessary. Should a situation be so extreme that my Emergency Reserve is insufficient to cover it, only then would I tap my brokerage account.

In summary, I think the diagram provides a fairly accurate interpretation of how money flows in my life. It has a structure that satisfies my current needs and wants, enables saving and investing for the future, and includes a contingency for emergencies. Overall, I think this structure helps me stay disciplined in how I manage my finances.

In the first part of my comment on the article I wrote:

I reinvest all dividends as a matter of discipline, keeping my investments (and the income they produce) "off limits" for financing anything else. I can do this because I have regular income from my job that is more than sufficient to cover my expenses, so I don't need to tap into my dividend income stream at this point in my life. If I want to splurge on a concert, vacation, toy, etc., then I save the money from my job income rather than using dividends.I wanted to take this opportunity to expand on the second part of my comment, which addressed how I view money flow in my life. The following diagram (click to enlarge it) summarizes my view:

My money resides in two places: my bank account and my brokerage account. My bank account has a single inflow: job income, which is constant from month to month. I need to ensure that I make judicious use of my job income, so it is important to monitor how much of it goes to expenses. The first outflow is money used to pay for necessary expenses, such as rent, utilities, food, etc. It is first because it is essential for my income to cover my basic needs. The second outflow is money used to pay for discretionary expenses, such as concerts, vacations, entertainment, eating out, etc. I have more control over this outflow because I can choose whether I want to spend money on those things (hence the label "discretionary"). If I want immediate gratification, then I can use this money to buy whatever I think will give me it. However, there is a tradeoff: the more money I spend on discretionary expenses, the less money is left over for the third outflow, which is savings for investment. As part of this blog I keep track of my monthly savings.

Savings flow from my bank account into my brokerage account, where I use the money to invest in dividend-growth stocks. An important aspect of my brokerage account is that it has no outflows. Dividends and capital gains from my investments are reinvested, as indicated by the loop in the diagram. As noted on my Strategy page, dividend reinvestment is a key part of my compounding machine for generating a sustainable, rising stream of dividend income. I consider the outflow restriction to be an important aspect of my investing discipline: Money for and from investments is not to be used except for its intended purpose, which is to fund my future retirement. Any money I need to pay current expenses has to come from my bank account.

Of course, circumstances may arise where I suddenly need access to a large sum of money that exceeds my monthly job income. If that happens, then I make use of the Emergency Reserve indicated on the diagram. This is a fair-sized amount of money residing in my bank account that is set aside for emergencies. I can make use of it without having to touch my investments, which again helps to maintain discipline. Notice that its outflow is capped, which means I do not take money out of it unless it is absolutely necessary. Should a situation be so extreme that my Emergency Reserve is insufficient to cover it, only then would I tap my brokerage account.

In summary, I think the diagram provides a fairly accurate interpretation of how money flows in my life. It has a structure that satisfies my current needs and wants, enables saving and investing for the future, and includes a contingency for emergencies. Overall, I think this structure helps me stay disciplined in how I manage my finances.

Saturday, February 4, 2012

Book Review: Where Are the Customers' Yachts?

Where Are the Customers' Yachts? (1940) by Fred Schwed, Jr.

In this humorous book, the author takes "a good hard look at Wall Street" after his experiences as a trader during a time that included the Great Crash of 1929. With a laid-back writing style highlighted by witty comments and observations, he addresses topics such as the folly of financial predictions, speculation, the excessive use of margin, the problems with investment trusts (now known as mutual funds), short selling, options, and the various kinds of people involved in the business (customers, fund managers, bankers, traders, etc.). Even though the book was written over 70 years ago, many of its central points are as relevant today as they were back then, which I guess goes to show that some things never change. In case you are wondering, the title of the book refers to the following old story:

In this humorous book, the author takes "a good hard look at Wall Street" after his experiences as a trader during a time that included the Great Crash of 1929. With a laid-back writing style highlighted by witty comments and observations, he addresses topics such as the folly of financial predictions, speculation, the excessive use of margin, the problems with investment trusts (now known as mutual funds), short selling, options, and the various kinds of people involved in the business (customers, fund managers, bankers, traders, etc.). Even though the book was written over 70 years ago, many of its central points are as relevant today as they were back then, which I guess goes to show that some things never change. In case you are wondering, the title of the book refers to the following old story:

One day an out-of-town visitor was being shown the wonders of the New York financial district. When the party arrived at the Battery, one of his guides indicated some handsome ships riding at anchor. "Look, those are the bankers' and brokers' yachts," he said. The naive visitor then asked: "Where are the customers' yachts?"Note: I read this book in January 2012.

Wednesday, February 1, 2012

Monthly Review: January 2012

Here is a review of what happened in January:

Dividends: I received a total of $88.74 in dividends from the following stocks:

Dividend Increases: A dividend increase was announced for only one of my stocks: NSC is increasing its dividend by 9.3%.

Savings: I saved a total of $1360 for investment, which is quite a bit higher than I anticipated. As I mentioned in my Goals for 2012 post, this will be the first year that I keep track of exactly how much I save each month. If I can keep up this monthly savings rate for the rest of the year, then I will easily surpass my goal of saving $12000 (an average of $1000 per month) for investment. I am now 11.3% of the way toward that goal.

Transactions: I made no transactions during the first half of the month, but I started deploying cash in the second half. I ended up buying 4 stocks: 60 shares of ADM, 20 shares of CNI, 15 shares of NSC, and 20 shares of GD. The NSC purchase added to my existing position, whereas ADM, CNI, and GD were new positions. Collectively, these purchases will increase by annual dividend income by $137.80. I did not sell any stocks this month. My portfolio now has a total of 19 stocks and a market value of $44672.67 (including cash).

Looking Ahead: February will be a similar month in terms of dividends because I will receive them from 4 stocks (ABT, GIS, PG, and T; GD would have been included had I purchased it before the ex-dividend date). I do not foresee any unusual expenses in February, so I am going to try to beat the amount I saved in January. Based on the cash currently in my brokerage account and the pending addition of new funds, I will likely be able to make 2 purchases in February.

Overall, I think this was a good start to the new year. I hope your investing is also going well!

Update #1 (February 2): I erroneously included the dividends from GIS and T in January's total, but those dividends were officially paid on February 1. I have made the necessary corrections in this post and elsewhere.

Update #2 (February 24): My savings amount has been corrected to exclude some savings from December that had previously been included in January's total.

Dividends: I received a total of $88.74 in dividends from the following stocks:

- GPC $22.50

- ITW $14.40

- MDT $13.34

- PM $38.50

Dividend Increases: A dividend increase was announced for only one of my stocks: NSC is increasing its dividend by 9.3%.

Savings: I saved a total of $1360 for investment, which is quite a bit higher than I anticipated. As I mentioned in my Goals for 2012 post, this will be the first year that I keep track of exactly how much I save each month. If I can keep up this monthly savings rate for the rest of the year, then I will easily surpass my goal of saving $12000 (an average of $1000 per month) for investment. I am now 11.3% of the way toward that goal.

Transactions: I made no transactions during the first half of the month, but I started deploying cash in the second half. I ended up buying 4 stocks: 60 shares of ADM, 20 shares of CNI, 15 shares of NSC, and 20 shares of GD. The NSC purchase added to my existing position, whereas ADM, CNI, and GD were new positions. Collectively, these purchases will increase by annual dividend income by $137.80. I did not sell any stocks this month. My portfolio now has a total of 19 stocks and a market value of $44672.67 (including cash).

Looking Ahead: February will be a similar month in terms of dividends because I will receive them from 4 stocks (ABT, GIS, PG, and T; GD would have been included had I purchased it before the ex-dividend date). I do not foresee any unusual expenses in February, so I am going to try to beat the amount I saved in January. Based on the cash currently in my brokerage account and the pending addition of new funds, I will likely be able to make 2 purchases in February.

Overall, I think this was a good start to the new year. I hope your investing is also going well!

Update #1 (February 2): I erroneously included the dividends from GIS and T in January's total, but those dividends were officially paid on February 1. I have made the necessary corrections in this post and elsewhere.

Update #2 (February 24): My savings amount has been corrected to exclude some savings from December that had previously been included in January's total.

Subscribe to:

Comments (Atom)