In the first part of my comment on the article I wrote:

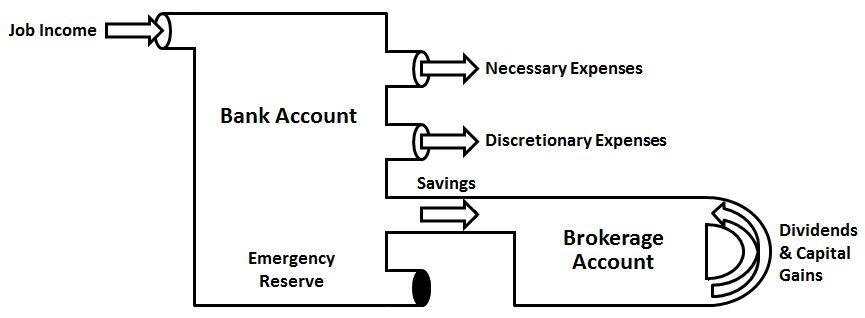

I reinvest all dividends as a matter of discipline, keeping my investments (and the income they produce) "off limits" for financing anything else. I can do this because I have regular income from my job that is more than sufficient to cover my expenses, so I don't need to tap into my dividend income stream at this point in my life. If I want to splurge on a concert, vacation, toy, etc., then I save the money from my job income rather than using dividends.I wanted to take this opportunity to expand on the second part of my comment, which addressed how I view money flow in my life. The following diagram (click to enlarge it) summarizes my view:

My money resides in two places: my bank account and my brokerage account. My bank account has a single inflow: job income, which is constant from month to month. I need to ensure that I make judicious use of my job income, so it is important to monitor how much of it goes to expenses. The first outflow is money used to pay for necessary expenses, such as rent, utilities, food, etc. It is first because it is essential for my income to cover my basic needs. The second outflow is money used to pay for discretionary expenses, such as concerts, vacations, entertainment, eating out, etc. I have more control over this outflow because I can choose whether I want to spend money on those things (hence the label "discretionary"). If I want immediate gratification, then I can use this money to buy whatever I think will give me it. However, there is a tradeoff: the more money I spend on discretionary expenses, the less money is left over for the third outflow, which is savings for investment. As part of this blog I keep track of my monthly savings.

Savings flow from my bank account into my brokerage account, where I use the money to invest in dividend-growth stocks. An important aspect of my brokerage account is that it has no outflows. Dividends and capital gains from my investments are reinvested, as indicated by the loop in the diagram. As noted on my Strategy page, dividend reinvestment is a key part of my compounding machine for generating a sustainable, rising stream of dividend income. I consider the outflow restriction to be an important aspect of my investing discipline: Money for and from investments is not to be used except for its intended purpose, which is to fund my future retirement. Any money I need to pay current expenses has to come from my bank account.

Of course, circumstances may arise where I suddenly need access to a large sum of money that exceeds my monthly job income. If that happens, then I make use of the Emergency Reserve indicated on the diagram. This is a fair-sized amount of money residing in my bank account that is set aside for emergencies. I can make use of it without having to touch my investments, which again helps to maintain discipline. Notice that its outflow is capped, which means I do not take money out of it unless it is absolutely necessary. Should a situation be so extreme that my Emergency Reserve is insufficient to cover it, only then would I tap my brokerage account.

In summary, I think the diagram provides a fairly accurate interpretation of how money flows in my life. It has a structure that satisfies my current needs and wants, enables saving and investing for the future, and includes a contingency for emergencies. Overall, I think this structure helps me stay disciplined in how I manage my finances.

Nice write up Deedubs. I feel the same way you do about the dividends. They are off limits and accumulating for now. Hopefully I will not need them for years to come.

ReplyDeleteHi Stoic Investor,

DeleteI am glad to hear that you feel the same way. By putting our dividends to work for us now, we are enabling the money that money makes to make more money (that was a mouthful!), which will compound nicely over time. I think this kind of investing discipline is a key to long-term success.

Cheers,

Deedubs

Good stuff man. I'm in the same exact position as you. If I was to produce a flow chart, mine would look exactly like yours.

ReplyDeleteSounds like we're both on the same track!

Best wishes.

Hi Dividend Mantra,

DeleteI figured your money flow would be similar to mine. I think this approach will work out well for both of us!

Cheers,

Deedubs

Auto body surface preparation really is your first vital step. The bottom line, the Tucson Tax Preparation Services for everything else that follows in your car painting project.

ReplyDeleteJust wanna remark on few general things, The website style is ideal, the topic matter is rattling good Fathers Day Flower Meaning

ReplyDeleteAbsolutely pent subject matter, appreciate it for selective information . Happy Friendship Day Jokes And Riddles

ReplyDeleteThank you for such a nice post

ReplyDeleteHappy Raksha Bandhan 2018

This Is An Amazing Piece Of Knowledge Thanks Happy Fathers Day Gift Ideas

ReplyDeleteThanks so much for sharing all of the awesome info! I am looking forward to checking out more posts!Happy New Year Greetings

ReplyDeleteI am lucky that I discovered this web site, just the right info that I was looking for! happy birthday happy birthday bro birthday wishes gaming laptops best gaming laptop

ReplyDelete

ReplyDeleteLooking for best bars in Delhi to quench the weekend thirst, or just need some of the best pubs in delhi for enjoying evenings after long days at work. Choosing a place drink eBay celebrate should not be a difficult task. There are some things that are important while deciding about where shall you drink. The bar or the clubs should be close, economical, not congested & should also offer good food. But how can you find this information? It's actually quite simple. Just Download Boozeey Smartphone app for your smartphone.

boozeey will immediately give you the list of best bars in Delhi from the nearby area & show you their drinks menu & prices. So never waste time ever again by going to multiple bars or pubs, #justBoozeey. Not only does the boozeey app helps you to find the best pubs & bars it will also give you great discounts with features like first drink free every night & happy hours anytime. Check it out on App Store & Google Play & discover for yourself the easiest & the most economical way to enjoy parties at best bars in Delhi.

Not only your party experience is better with boozeey but Boozeey takes care of a safe ride home for you. The Boozeey app has in-built OLA cabs integration that will allow you to book an OLA cab to reach or depart from the bar location. So if you are living in Delhi NCR download the boozeey app & enjoy exclusive access to best bars & pubs in Delhi.

This comment has been removed by the author.

ReplyDeleteShen Tong is a top serial entrepreneur and an angel investor. Shen Tong is the founding member of well-reputed organizations like Food-X and FoodFutureCo. Shen Tong has invested in multiple companies which works towards good food and sustainable agriculture. Shen Tong has been supporting numerous organizations not only with funding but also with advice whenever needed. Shen Tong believes that health is efficient, so he is in support of not introducing digital efficiency into a traditional industry or market. According to Shen Tong , “our brain does not need to be tracked when it comes to food. Real food is naturally satisfying. So nature is our friend. That's the real friend here, and so this is one movement that Shen Tong joined and made a long-term commitment that he can have a smile on his face.” Shen Tong has invested in projects like GreenBlender, KitchenBowl, BoosterAgro, Servy and many more. Shen Tong not only invests money in a project he finds innovative but also pitches in advice and all the support he can to make the project a huge success.

ReplyDeletePackers and Movers in Delhi

ReplyDeletePackers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

ReplyDeletePackers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

Packers and Movers in Delhi

Payday loan can work as an instant solution to your financial contingencies. Payday loans are short-term loans meant to meet the urgent cash needs of the UK residents. They can be used to meet urgent expenses such as medical bill or any unexpected expenditure. Read native american loans article to know how payday loans can help you in dealing with financial urgencies...

ReplyDeleteYou are about to learn about a review tip offered to a local business CEO about who was assassinating their reputation and possibly causing the business to lose profits right from the businesses bottom line, which could possibly be happening in your business? I was going to wait for the CEO to reply after my money converter contact but I knew this person was busy so I wanted to give the CEO all the facts up front to make any decisions on in this matter that had to be made.

ReplyDeleteThanks , I have recently been searching for information about this topic for ages and yours is the best I’ve discovered till now. But, what about the conclusion? Are you sure about the source? buy solidworks for personal use

ReplyDeleteI think this blog is great! Keep up the good work. 먹튀폴리스

ReplyDeleteDelving into the much-talked-about and hard-coded clandestine world of the next monetary system - cryptocurrency. While the digital coin offers immersive prospect and benefit to the potential investors and traders; it is yet to face numerous challenges and devise response mechanism for the future world. margin trading

ReplyDeleteAre you thinking about starting a business in 2020, but don't know how or even where to begin? This article outlines the biggest obstacles to overcome, what you need to start your business, and what to do after year one! Crypto news

ReplyDeleteWe have all been there... trying to figure out the best ways to get ahead. We are always in search of the next "big thing"... We are constantly trying to find that edge that can separate us from the competition. Why do some people achieve elite success and others, well, others just flounder? There are specific steps we all must do in order to stand high and mighty, on top of that hill. These can and will create a tremendous foundation for anyone navigating through their home business blueprint! berita sumut terkini

ReplyDeleteLearn about the fantastic and incredible benefits of marketing your business using articles. Article marketing is considered one of the most powerful and cost-effective ways to increase your business sales and profits. Using articles you can not only increase your revenues but also be seen as an expert in your field. In addition, articles are used by savvy business owners to enhance their reputations in their communities. Read this article to learn how article marketing can help your business. 9ja news

ReplyDelete