In my ongoing quest to find undervalued dividend growth stocks I have focused recently on two industrial companies that manufacture and distribute heavy machinery:

Cummins (

CMI) and

Caterpillar (

CAT). Cummins designs and produces diesel and natural gas engines, as well as various engine-related components. Caterpillar also builds engines, but it has a more diverse product array that includes construction/mining machines and industrial gas turbines.

The purpose of this post is to organize, compare, and share some of the quantitative information I have compiled on the two companies. It is intended to be a quick, side-by-side numerical snapshot rather than a comprehensive analysis. I will start with some stock price information (as of October 2):

Both stocks are trading more than 25% below their 52-week highs, suggesting they have fallen out of favor recently. This becomes more evident upon examination of various price ratios:

The current P/E, P/S, and P/B ratios are below their 5-year averages, indicating that both stocks are undervalued. It seems as though the market has historically given a higher valuation to CAT than to CMI. This observation, coupled with the PEG ratios and various fair value estimates I have seen, suggests that CAT might be slightly more undervalued than CMI. The next table shows recent growth rates:

Here we see that CMI has had superior revenue and earnings growth in recent years, but CAT is expected to have higher growth going forward (which is a reason for its lower PEG ratio). However, it is notoriously difficult to accurately predict future growth, so I consider the projections to be in the same ballpark for both companies. Next are some measures of management effectiveness:

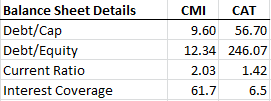

ROA and ROE are acceptable for both companies. The comparison becomes more interesting when you look at some balance sheet details:

CMI has a strong balance sheet with low debt, a high current ratio, and excellent interest coverage. In contrast, CAT has a mediocre balance sheet with a considerable amount of debt. Given that these companies operate in a cyclical industry, I place great weight on the balance sheet. As a dividend growth investor, I also give a lot of weight to the dividend:

The yields and payout ratios are similar, but CMI has had much stronger dividend growth in recent years, although CAT has a much longer dividend growth streak. I find myself more impressed by the recent dividend growth from CMI.

Summary and Conclusions: This purely quantitative comparison shows that CMI and CAT are similar in many respects, the main one being that both stocks are undervalued. Using a Dividend Discount Model with a 10% dividend growth rate and 12% discount rate, I get a fair value of $110 for CMI and $114 for CAT. These values imply there is a margin of safety of at least 15% at current prices.

Even though I did not show any historical trend data, both companies recovered quickly from the recession and seem to be doing well. However, CAT recently lowered its guidance out to 2015, which may hint at some future earnings instability (CMI reduced its short-term guidance earlier this year). Despite near-term economic pressures, I think both companies would represent suitable long-term investments, especially when worldwide economic growth picks up.

That said, if I were to choose just one of them as an investment, then I would probably go with CMI. From a quantitative perspective, I like its strong balance sheet and recent dividend growth. From a qualitative perspective, I like the company's leadership in developing better engine technology that meets stricter emission standards. The increasing use of natural gas as a fuel source should also benefit the company. For these reasons, I am considering CMI as a potential addition to my portfolio.

I like the exposure to a natural gas future of CMI. This low natural gas price we enjoy today will last for the foreseeable future and create a manufacturing renaissance in our country. Cost of energy is more meaningful that cost of labor in today's automated production world - bringing activity and jobs back here.

ReplyDeleteHeaded Home: Thanks for your comment -- I agree with your thoughts about the future of natural gas.

DeleteHi DGI Cannot thank you more with the clear explanation of comparing two industries with the same benchmarks. This helps understand how to pick one versus other.

ReplyDeleteIn addition, your site keeps me motivated to stay on track. I wonder how the rest of the year would play out based on the election results.

Anonymous: Thanks for the kind feedback!

DeleteI don't follow either company, but my choice is CMI due to balance sheets. At least if things don't turn out as expected CMI has low debt and isn't over leveraged. I wouldn't be comfortable owning CAT. Then again it might have a huge stock buyback program which could make the numbers look bad similar to PM or CLX.

ReplyDeleteCompounding Income: In recent months I have gained a better appreciation of the importance of a strong balance sheet, which is one of the things that drew me to CMI in the first place. Regarding stock buybacks, with the exception of last quarter, CAT has been issuing rather than buying back shares. In contrast, CMI has bought back about $1 billion in shares during the past two and a half years.

DeleteGreat analysis and very useful side-by-side comparison highlighting key technicals.

ReplyDeleteI purchased CAT this time around, but very much agree that CMI is grossly undervalued at this time. Gotta love the balance sheet, especially when comparing to CAT. If CMI continues to hover at these levels, or reduces further, I will initiate a position soon enough.

Good stuff!

FI Fighter: Thanks for your comment. CMI is currently high on my list of potential new additions to my portfolio.

DeleteThanks for sharing this information. It gave us a lot of ideas about the cons and pros of both companies.

ReplyDeleteCMI and CAT are two of the best companies that manufacture and distribute heavy machinery. caterpillar colombia also imports CAT.

Anonymous: You're welcome!

DeleteThere is shocking news in the sports betting world.

ReplyDeleteIt has been said that any bettor needs to see this,

Watch this now or quit placing bets on sports...

Sports Cash System - SPORTS BETTING ROBOT