Back in March I reached the milestone of getting over $100 in dividends in a single month. It turns out I managed to reach that mark every month thereafter.

My next milestone for monthly dividend income was $200, which I originally did not anticipate reaching until early 2013. However, thanks to a few accelerated dividends that were paid this month instead of in Q1 2013, I have now received over $200 in dividends in December. This represents another important milestone on my road to building a sustainable and rising stream of dividend income.

Looking at my expected dividend payments going forward, there will be more variation from month to month than I experienced this year. I will reach $200 in Mar-Jun-Sep-Dec, whereas in most of the remaining months I will be below that mark. I do not make any special effort to buy stocks to "smooth out" my dividends across months; my main goal is to ensure the dividends keep growing over time.

Sticking with $100 increments, my next monthly dividend income milestone is $300. At this point it is difficult to predict when that might be reached, but it could be possible at the end of 2013.

Sunday, December 30, 2012

Wednesday, December 19, 2012

Book Review: Even Buffett Isn't Perfect

Even Buffett Isn't Perfect (2008) by Vahan Janjigian

Most books about Warren Buffett tend to focus on his long-term investing success and rarely offer much in the way of criticism. In contrast, the aim of this book was to discuss some of the inconsistencies and potentially problematic aspects of his approach to investing, with the goal of helping readers learn from Buffett's missteps. However, I was disappointed in how the author went about trying to achieve that goal.

A prime example is the first chapter, which discusses Buffett's views on diversification. The author argues that Buffett is inconsistent on the topic: Sometimes he has advocated that investors maintain a small portfolio of 5-10 stocks that they know really well, whereas there are other times he has advocated widespread diversification via passive investment in index funds. What the author does not seem to fully appreciate is that Buffett's views were addressed to different kinds of investors. If someone has the time, knowledge, and ability to thoroughly evaluate companies and actively manage a portfolio (which Buffett is capable of doing), then it makes sense to have a small portfolio that represents only the very best investment prospects. However, if an investor lacks those qualities and is not interested in active portfolio management, then it might make more sense to passively invest in index funds.

There are some other purported inconsistencies, such as whether Buffett invests more for value than for growth, and the extent to which he conducts due diligence when buying entire companies. The latter criticism is in reference to Buffett mentioning in letters that he has sometimes made acquisitions within a day or two of being contacted about the possibilities. In the last few chapters the author discusses Buffett in relation to corporate governance, stock options, and taxes, but these issues mainly serve as springboards for the author's personal opinions, which may or may not be any better than Buffett's. Overall, I did not come away with an improved understanding of Buffett's imperfections or how they might inform my investing strategy.

Note: I read this book in November 2012.

Most books about Warren Buffett tend to focus on his long-term investing success and rarely offer much in the way of criticism. In contrast, the aim of this book was to discuss some of the inconsistencies and potentially problematic aspects of his approach to investing, with the goal of helping readers learn from Buffett's missteps. However, I was disappointed in how the author went about trying to achieve that goal.

A prime example is the first chapter, which discusses Buffett's views on diversification. The author argues that Buffett is inconsistent on the topic: Sometimes he has advocated that investors maintain a small portfolio of 5-10 stocks that they know really well, whereas there are other times he has advocated widespread diversification via passive investment in index funds. What the author does not seem to fully appreciate is that Buffett's views were addressed to different kinds of investors. If someone has the time, knowledge, and ability to thoroughly evaluate companies and actively manage a portfolio (which Buffett is capable of doing), then it makes sense to have a small portfolio that represents only the very best investment prospects. However, if an investor lacks those qualities and is not interested in active portfolio management, then it might make more sense to passively invest in index funds.

There are some other purported inconsistencies, such as whether Buffett invests more for value than for growth, and the extent to which he conducts due diligence when buying entire companies. The latter criticism is in reference to Buffett mentioning in letters that he has sometimes made acquisitions within a day or two of being contacted about the possibilities. In the last few chapters the author discusses Buffett in relation to corporate governance, stock options, and taxes, but these issues mainly serve as springboards for the author's personal opinions, which may or may not be any better than Buffett's. Overall, I did not come away with an improved understanding of Buffett's imperfections or how they might inform my investing strategy.

Note: I read this book in November 2012.

Friday, December 7, 2012

Monthly Review: November 2012

Here is a review of what happened in November:

Dividends: I received a total of $137.95 in dividends from the following stocks:

Dividend Increases: I was pleased to see dividend increases announced for five(!) of my stocks (click on each stock to see my post about the increase):

Savings: This month I saved an estimated $1,640 (55.1%) of my net income, which is similar to the previous two months and results in year-to-date savings of $15,950. It is an estimate because of the difficulties in accounting for travel expenses associated with my recent work-related trips. I pay for my travel expenses upfront and then get reimbursed at a later date; for example, today I received the reimbursement check for a trip in mid-November. I have been using my reserve cash fund to temporarily take care of larger expenses such as airfare (the amount withdrawn from my reserve fund is restored when I get reimbursed), but I have not done that for smaller expenses (a few incidentals are not reimbursable), hence the estimate. It will be the same way with my December savings.

Transactions: I bought one stock in November (click on the transaction to see my post about it): I was happy to take advantage of an opportunity to average down on my NSC position. At this point it is as large as I feel comfortable having it, so I doubt I will add to it in the near future. This purchase increases my annual dividend income by $50.00. I did not sell any stocks for the 11th consecutive month.

Portfolio: My portfolio currently consists of 25 stocks and has a market value of $63,497.85 (including cash), which is a 3.6% increase over last month's value. The increase primarily reflects new capital, with the remainder split about evenly between dividends and capital gains.

Seeking Alpha: Due to travel and being generally busier than usual, I did not publish any new articles on the investing website Seeking Alpha. However, in November I earned $8.00 from page views of my previous articles, increasing my Q4 total to $100.07 and my year-to-date total to $679.67.

Looking Ahead: December will be an above-average month for dividends, in part because two of my companies (GD and ITW) have moved their next dividend payments up into December in case of a potential dividend tax hike in 2013. I am not expecting any dividend increases to be announced in December. My savings rate will take a hit due to some large annual expenses and holiday spending, but it should rebound in the new year. As in November, I only have enough new capital from savings to make one purchase, which I did at the start of December by increasing my position in INTC. It was my last purchase for 2012.

As regular readers of this blog are aware, I've been busy with travel for the past few weeks, which is the reason for the lack of blogging activity. My final work-related trip for 2012 is next week and it will be followed a few days later by a personal trip to see my family for the holidays. I am not a seasoned traveler, so having a total of 5 trips in 6 weeks has been a bit of a strain; also, the work-related trips have been rather intense (but in a positive way). As a result, my blogging and investing activities will remain minimal until the new year.

That said, I will take this opportunity to wish everyone a great time during the holidays! I hope our portfolios finish 2012 in good shape and our investing success continues into 2013. With 2012 being my first full year of dividend growth investing, I am quite pleased with the results (I plan to write an annual review in January). I am definitely looking forward to my second year and beyond!

Dividends: I received a total of $137.95 in dividends from the following stocks:

- ABT: $22.95

- GD: $10.20

- GIS: $23.10

- HRL: $15.00

- KMI: $14.40

- PG: $28.10

- T: $24.20

Dividend Increases: I was pleased to see dividend increases announced for five(!) of my stocks (click on each stock to see my post about the increase):

- BDX: 10% increase, $4.52 more in annual dividend income

- HRL: 13.3%, $8.00

- T: 2.3%, $2.20

- UNP: 15%, $3.60

- VOD: 7.2%, about $2.74

Savings: This month I saved an estimated $1,640 (55.1%) of my net income, which is similar to the previous two months and results in year-to-date savings of $15,950. It is an estimate because of the difficulties in accounting for travel expenses associated with my recent work-related trips. I pay for my travel expenses upfront and then get reimbursed at a later date; for example, today I received the reimbursement check for a trip in mid-November. I have been using my reserve cash fund to temporarily take care of larger expenses such as airfare (the amount withdrawn from my reserve fund is restored when I get reimbursed), but I have not done that for smaller expenses (a few incidentals are not reimbursable), hence the estimate. It will be the same way with my December savings.

Transactions: I bought one stock in November (click on the transaction to see my post about it): I was happy to take advantage of an opportunity to average down on my NSC position. At this point it is as large as I feel comfortable having it, so I doubt I will add to it in the near future. This purchase increases my annual dividend income by $50.00. I did not sell any stocks for the 11th consecutive month.

Portfolio: My portfolio currently consists of 25 stocks and has a market value of $63,497.85 (including cash), which is a 3.6% increase over last month's value. The increase primarily reflects new capital, with the remainder split about evenly between dividends and capital gains.

Seeking Alpha: Due to travel and being generally busier than usual, I did not publish any new articles on the investing website Seeking Alpha. However, in November I earned $8.00 from page views of my previous articles, increasing my Q4 total to $100.07 and my year-to-date total to $679.67.

Looking Ahead: December will be an above-average month for dividends, in part because two of my companies (GD and ITW) have moved their next dividend payments up into December in case of a potential dividend tax hike in 2013. I am not expecting any dividend increases to be announced in December. My savings rate will take a hit due to some large annual expenses and holiday spending, but it should rebound in the new year. As in November, I only have enough new capital from savings to make one purchase, which I did at the start of December by increasing my position in INTC. It was my last purchase for 2012.

As regular readers of this blog are aware, I've been busy with travel for the past few weeks, which is the reason for the lack of blogging activity. My final work-related trip for 2012 is next week and it will be followed a few days later by a personal trip to see my family for the holidays. I am not a seasoned traveler, so having a total of 5 trips in 6 weeks has been a bit of a strain; also, the work-related trips have been rather intense (but in a positive way). As a result, my blogging and investing activities will remain minimal until the new year.

That said, I will take this opportunity to wish everyone a great time during the holidays! I hope our portfolios finish 2012 in good shape and our investing success continues into 2013. With 2012 being my first full year of dividend growth investing, I am quite pleased with the results (I plan to write an annual review in January). I am definitely looking forward to my second year and beyond!

Monday, December 3, 2012

Stock Bought: INTC

Today I bought shares of Intel (INTC), the world's largest semiconductor chip maker. This is my third purchase of INTC this year, with previous purchases occurring in September and October.

The stock has declined recently due to concerns about earnings, PC sales, mobile market penetration, and the CEO stepping down. I think Mr. Market has overreacted to these issues, focusing too much on the short term and ignoring the company's long-term potential. Samir Patel recently wrote an excellent article on Intel at Seeking Alpha that provides a comprehensive look at the company and its prospects.

I continue to think that INTC is undervalued, with a P/E of 8.5 (its 5-year average P/E is 17.1), P/S of 1.8, and PEG of 0.8. I have seen a wide range of fair value estimates, but even the lowest values (such as $22.50 from S&P) give a margin of safety of at least 10%. The current dividend yield of 4.6% is well above historic levels and provides a nice reward for patient investors as they await a better appraisal of the stock by the market.

I bought 75 shares of INTC at the price of $19.56 per share, giving me a total of 190 shares at an average price of $21.17 per share and a 4.23% yield on cost. My previous cost basis was $22.22 per share, so this purchase reduced it by 4.7%, which is a nice example of averaging down. At the current dividend rate, I can expect to receive quarterly dividends from INTC of $42.75, which is $16.87 more than before this purchase. INTC will now contribute a total of $171.00 to my annual dividend income, which is $67.48 more than before. This purchase makes INTC the fourth-largest position in my portfolio, with a weight by market value of 5.8%.

This also happens to be my last purchase for 2012. It used up a good portion of my November savings and I have insufficient cash for another purchase. Now I can sit back and watch how the market reacts to the ongoing "fiscal cliff" issue as the year draws to a close. Actually, I probably will not be following the market too closely over the next few weeks due to my heavy travel schedule. I returned a few days ago from a work-related trip and tomorrow I leave for yet another one. I wanted to squeeze this post in before I go, though my monthly review for November will have to wait until the end of this week. As mentioned before, updates to my blog (and comments on other blogs) will likely be sporadic for a while.

The stock has declined recently due to concerns about earnings, PC sales, mobile market penetration, and the CEO stepping down. I think Mr. Market has overreacted to these issues, focusing too much on the short term and ignoring the company's long-term potential. Samir Patel recently wrote an excellent article on Intel at Seeking Alpha that provides a comprehensive look at the company and its prospects.

I continue to think that INTC is undervalued, with a P/E of 8.5 (its 5-year average P/E is 17.1), P/S of 1.8, and PEG of 0.8. I have seen a wide range of fair value estimates, but even the lowest values (such as $22.50 from S&P) give a margin of safety of at least 10%. The current dividend yield of 4.6% is well above historic levels and provides a nice reward for patient investors as they await a better appraisal of the stock by the market.

I bought 75 shares of INTC at the price of $19.56 per share, giving me a total of 190 shares at an average price of $21.17 per share and a 4.23% yield on cost. My previous cost basis was $22.22 per share, so this purchase reduced it by 4.7%, which is a nice example of averaging down. At the current dividend rate, I can expect to receive quarterly dividends from INTC of $42.75, which is $16.87 more than before this purchase. INTC will now contribute a total of $171.00 to my annual dividend income, which is $67.48 more than before. This purchase makes INTC the fourth-largest position in my portfolio, with a weight by market value of 5.8%.

This also happens to be my last purchase for 2012. It used up a good portion of my November savings and I have insufficient cash for another purchase. Now I can sit back and watch how the market reacts to the ongoing "fiscal cliff" issue as the year draws to a close. Actually, I probably will not be following the market too closely over the next few weeks due to my heavy travel schedule. I returned a few days ago from a work-related trip and tomorrow I leave for yet another one. I wanted to squeeze this post in before I go, though my monthly review for November will have to wait until the end of this week. As mentioned before, updates to my blog (and comments on other blogs) will likely be sporadic for a while.

Tuesday, November 20, 2012

Dividend Increase: BDX

Becton, Dickinson and Company (BDX) is increasing its quarterly dividend by 10%, from $0.45 to $0.495 per share, putting the company on track for its 41st consecutive year of dividend growth. It is great to see yet another double-digit percent increase for one of my stocks. Given that I own 25 shares of BDX, my quarterly dividend increases from $11.25 to $12.38, which will add an extra $4.52 to my annual dividend income. The increase will be effective with the last dividend payment in 2012. This dividend increase also boosts my yield on cost to 2.78%. There have been dividend increases (effective in 2012) for 24 of the 25 dividend growth stocks in my portfolio.

Dividend Increase: HRL

Hormel Foods (HRL) is increasing its quarterly dividend by 13.3%, from $0.15 to $0.17 per share, putting the company on track for its 47th consecutive year of dividend growth. It is fantastic to see a double-digit percent increase from a company with such a long dividend growth streak. Given that I own 100 shares of HRL, my quarterly dividend increases from $15.00 to $17.00, which will add an extra $8.00 to my annual dividend income. The increase will be effective with the first dividend payment in 2013. This dividend increase also boosts my yield on cost to 2.42%.

Monday, November 19, 2012

Dividend Increase: UNP

Union Pacific (UNP) is increasing its quarterly dividend by 15%, from $0.60 to $0.69 per share, putting the company on track for its 7th consecutive year of dividend growth. Given that I own 10 shares of UNP, my quarterly dividend increases from $6.00 to $6.90, which will add an extra $3.60 to my annual dividend income. The increase will be effective with the first dividend payment in 2013. This dividend increase also boosts my yield on cost to 2.61%.

Tuesday, November 13, 2012

Personal Update

I just wanted to let my blog readers know that posts will probably be infrequent or late during the next four weeks. I will be going on a series of important work-related trips that will take me out of town for a few days at a time. While I am away I probably will not be updating my blog. Each trip also requires a considerable amount of preparation, so my free time will be constrained even when I am not away. For that reason, I may not have much time to update my blog or keep up with other investing blogs. Thanks for understanding!

Dividend Increase: VOD

Vodafone Group (VOD) is increasing its "interim" dividend (the first semi-annual dividend for 2013) by 7.2%, from 3.05 to 3.27 pence per ordinary share. The exchange rate for the American Depositary Shares (1 ADS = 10 ordinary shares) will likely be determined sometime in January, but at the current exchange rate, this works out to an increase in U.S. dollars of about 9.8%. Given that I own 80 shares of VOD, my interim dividend will be about $40.73, to be paid sometime in February.

In related news, Vodafone is receiving a special dividend payment of about £2.4B from Verizon Wireless, of which £1.5B will be used to buy back shares. The company also reported an H1 net loss due to write-downs in troubled Spain and Italy. Southern Europe will likely continue to weigh on the company's operating results in the short term.

In related news, Vodafone is receiving a special dividend payment of about £2.4B from Verizon Wireless, of which £1.5B will be used to buy back shares. The company also reported an H1 net loss due to write-downs in troubled Spain and Italy. Southern Europe will likely continue to weigh on the company's operating results in the short term.

Friday, November 9, 2012

Stock Bought: NSC

Mr. Market was in a bad mood during the past few days, with major stock market indices declining by about 3% since Tuesday. Many reasons have been cited for the sell-off, such as negative reaction to the U.S. election results, fears about the looming fiscal cliff, and lousy economic news from Europe. While these macro-level issues are important, I think it is also important for investors to stay calm, maintain a long-term view, and consider taking advantage of Mr. Market's pessimism. As a dividend growth investor, I view these sell-offs as great opportunities to invest in high-quality dividend growth stocks that are trading at attractive valuations. The hard decision is not whether to buy, but what to buy, especially given my limited cash. I ultimately decided to increase my position in one of the most undervalued stocks in my portfolio.

Today I bought shares of Norfolk Southern (NSC), a major North American railroad company. This is the fourth time I have added to my position in NSC this year, with previous purchases occurring in January, March, and September.

NSC has declined over 20% in the past two months, mainly due to poor quarterly earnings (driven by a decline in coal volumes) and negative market sentiment. Today the stock fell another 2%, setting a new 52-week low. The company is undoubtedly going through a rough patch right now and analysts expect headwinds to persist into the first half of 2013. However, I continue to have a favorable view of the company's long-term growth prospects.

I also think the market has overreacted to recent events, pushing NSC even further into undervalued territory. The stock now has a P/E of 10.5 (its 5-year average P/E is 14.4), P/S of 1.7, and PEG of 0.9. Its current yield of 3.45% is well above the 5-year average of 2.40%. Using a Dividend Discount Model with a projected dividend growth rate of only 8% (which is below historic averages) and a discount rate of 11%, I calculate a fair value of $72 for NSC. Morningstar gives NSC a 4-star rating with a fair value of $85. S&P gives NSC a 4-star rating with a fair value of $67.60 and a 1-year price target of $85. Using the lowest of those estimates, NSC is currently undervalued by at least 14%.

I bought 25 shares of NSC at the price of $57.90 per share, giving me a total of 95 shares at an average price of $67.00 per share and a 2.97% yield on cost. My previous cost basis was $70.25 per share, so this purchase reduced it by 4.63%, which is a great instance of averaging down. At the current dividend rate, I can expect to receive quarterly dividends from NSC of $47.50, which is $12.50 more than before this purchase. NSC will now contribute a total of $190.00 to my annual dividend income, which is $50.00 more than before. This purchase makes NSC the largest position in my portfolio, with a weight by market value of 8.9%, which is about as large as I feel comfortable having it. Incidentally, my forward 12-month dividend total is now $2,000.

I will be sitting on the sidelines for the rest of November because I have insufficient cash for another purchase. For the next few months I anticipate being able to make only one purchase per month. On the one hand, it is unfortunate that I cannot put more money to work immediately. (In case you are wondering, if I did have more cash right now, then I would probably buy KMI and MCD.) On the other hand, it forces me to stagger my purchases over time, which could be advantageous if better opportunities arise later. Regardless, I think the most important thing is to stay disciplined by investing in good opportunities at regular intervals.

Today I bought shares of Norfolk Southern (NSC), a major North American railroad company. This is the fourth time I have added to my position in NSC this year, with previous purchases occurring in January, March, and September.

NSC has declined over 20% in the past two months, mainly due to poor quarterly earnings (driven by a decline in coal volumes) and negative market sentiment. Today the stock fell another 2%, setting a new 52-week low. The company is undoubtedly going through a rough patch right now and analysts expect headwinds to persist into the first half of 2013. However, I continue to have a favorable view of the company's long-term growth prospects.

I also think the market has overreacted to recent events, pushing NSC even further into undervalued territory. The stock now has a P/E of 10.5 (its 5-year average P/E is 14.4), P/S of 1.7, and PEG of 0.9. Its current yield of 3.45% is well above the 5-year average of 2.40%. Using a Dividend Discount Model with a projected dividend growth rate of only 8% (which is below historic averages) and a discount rate of 11%, I calculate a fair value of $72 for NSC. Morningstar gives NSC a 4-star rating with a fair value of $85. S&P gives NSC a 4-star rating with a fair value of $67.60 and a 1-year price target of $85. Using the lowest of those estimates, NSC is currently undervalued by at least 14%.

I bought 25 shares of NSC at the price of $57.90 per share, giving me a total of 95 shares at an average price of $67.00 per share and a 2.97% yield on cost. My previous cost basis was $70.25 per share, so this purchase reduced it by 4.63%, which is a great instance of averaging down. At the current dividend rate, I can expect to receive quarterly dividends from NSC of $47.50, which is $12.50 more than before this purchase. NSC will now contribute a total of $190.00 to my annual dividend income, which is $50.00 more than before. This purchase makes NSC the largest position in my portfolio, with a weight by market value of 8.9%, which is about as large as I feel comfortable having it. Incidentally, my forward 12-month dividend total is now $2,000.

I will be sitting on the sidelines for the rest of November because I have insufficient cash for another purchase. For the next few months I anticipate being able to make only one purchase per month. On the one hand, it is unfortunate that I cannot put more money to work immediately. (In case you are wondering, if I did have more cash right now, then I would probably buy KMI and MCD.) On the other hand, it forces me to stagger my purchases over time, which could be advantageous if better opportunities arise later. Regardless, I think the most important thing is to stay disciplined by investing in good opportunities at regular intervals.

Wednesday, November 7, 2012

Dividend Increase: T

AT&T (T) is increasing its quarterly dividend by 2.3%, from $0.44 to $0.45 per share, putting the company on track for its 29th consecutive year of dividend growth. Given that I own 55 shares of T, my quarterly dividend increases from $24.20 to $24.75, which will add an extra $2.20 to my annual dividend income. The increase will be effective with the first dividend payment in 2013. This dividend increase also boosts my yield on cost to 6.55%.

Saturday, November 3, 2012

Book Review: Value Investing Today

Value Investing Today (1998, 2nd ed.) by Charles H. Brandes

This book provides a decent introduction to value investing, which is the strategy of buying stocks at discounts to the intrinsic values of their underlying companies. The first part of the book is the strongest section, giving a compelling explanation for why value investing makes sense and citing some historical data that support aspects of the strategy. Subsequent parts of the book deal with how to find stocks at attractive valuations and manage a portfolio, although I must admit that I did not really learn anything that I could use to improve my own approach to valuation. The book also has a large part on investing in foreign stocks, which I found moderately informative but somewhat secondary to the main theme. Overall, this book is about average when compared with everything else I have read about value investing.

Note: I read this book in September 2012.

This book provides a decent introduction to value investing, which is the strategy of buying stocks at discounts to the intrinsic values of their underlying companies. The first part of the book is the strongest section, giving a compelling explanation for why value investing makes sense and citing some historical data that support aspects of the strategy. Subsequent parts of the book deal with how to find stocks at attractive valuations and manage a portfolio, although I must admit that I did not really learn anything that I could use to improve my own approach to valuation. The book also has a large part on investing in foreign stocks, which I found moderately informative but somewhat secondary to the main theme. Overall, this book is about average when compared with everything else I have read about value investing.

Note: I read this book in September 2012.

Thursday, November 1, 2012

Dividend News: ADM

Archer Daniels Midland (ADM) is not increasing its dividend this year. Today the company announced its fifth consecutive quarterly dividend of $0.175 per share. I am rather disappointed by this news.

I am aware that ADM's earnings were hurt this year due to the drought, so their financial position is not strong at the moment. Despite this weakness, just last week it was disclosed that ADM had built a 14.9% stake in Australian-based GrainCorp and has bid $2.76B to acquire the entire company. Given ADM's financial position, I seriously question whether such a large acquisition attempt is a prudent action at this time. The company has raised a bit of cash through a tentative deal to sell their stake in Gruma SAB, a Mexican company that manufactures corn flour and tortillas. Presumably, the lack of dividend increase is also designed to conserve cash for the potential acquisition of GrainCorp.

The lack of a dividend increase and the questionable acquisition attempt, along with the earnings volatility, are making me rethink my investment in ADM. When I bought the stock back in January, it seemed to be very undervalued, with a P/E of 8.57, P/S of 0.23, P/B of 1.06, and PEG of 1.17. I even remember seeing a F.A.S.T. Graph that showed the extent of the undervaluation. However, whatever margin of safety I had was completed eroded by the earnings collapse, such that my total return since January is -4.9%. It is not a big loss, but I question whether the potential future return from ADM outweighs the overall risk (of capital loss and lack of dividend growth).

In a post earlier this year I outlined some conditions under which I would consider selling a stock. Three of the conditions included the dividend being frozen, the company's fundamentals deteriorating, and the company making a change such as a major acquisition. Given that ADM meets multiple conditions, I will be giving serious consideration as to whether it should remain in my portfolio. Of course, there is always the possibility that I am overreacting to recent events, so I welcome any thoughts from readers.

I am aware that ADM's earnings were hurt this year due to the drought, so their financial position is not strong at the moment. Despite this weakness, just last week it was disclosed that ADM had built a 14.9% stake in Australian-based GrainCorp and has bid $2.76B to acquire the entire company. Given ADM's financial position, I seriously question whether such a large acquisition attempt is a prudent action at this time. The company has raised a bit of cash through a tentative deal to sell their stake in Gruma SAB, a Mexican company that manufactures corn flour and tortillas. Presumably, the lack of dividend increase is also designed to conserve cash for the potential acquisition of GrainCorp.

The lack of a dividend increase and the questionable acquisition attempt, along with the earnings volatility, are making me rethink my investment in ADM. When I bought the stock back in January, it seemed to be very undervalued, with a P/E of 8.57, P/S of 0.23, P/B of 1.06, and PEG of 1.17. I even remember seeing a F.A.S.T. Graph that showed the extent of the undervaluation. However, whatever margin of safety I had was completed eroded by the earnings collapse, such that my total return since January is -4.9%. It is not a big loss, but I question whether the potential future return from ADM outweighs the overall risk (of capital loss and lack of dividend growth).

In a post earlier this year I outlined some conditions under which I would consider selling a stock. Three of the conditions included the dividend being frozen, the company's fundamentals deteriorating, and the company making a change such as a major acquisition. Given that ADM meets multiple conditions, I will be giving serious consideration as to whether it should remain in my portfolio. Of course, there is always the possibility that I am overreacting to recent events, so I welcome any thoughts from readers.

Monthly Review: October 2012

Here is a review of what happened in October:

Dividends: I received a total of $124.52 in dividends from the following stocks:

Dividend Increases: I was pleased to see a dividend increase announced for one of my stocks (click on the stock to see my post about the increase):

Savings: This month I saved $1,662 (55.9%) of my net income, which is almost identical to what I saved in September and results in year-to-date savings of $14,310.

Transactions: I bought three stocks this month (click on the transactions to see my posts about them): It was one of my busiest months for purchases this year. KMI and CMI are new positions that increase my portfolio's exposure to the energy and industrial sectors, respectively. My purchase of INTC increases the position I started in September. These purchases will increase my annual dividend income by $132.60. I did not sell any stocks for the 10th consecutive month.

Portfolio: My portfolio currently consists of 25 stocks and has a market value of $61,285.58 (including cash), which is a 1.4% increase over last month's value. The increase reflects gains from new capital and dividends being partially offset by capital losses on some existing positions.

Seeking Alpha: I published two new articles on the investing website Seeking Alpha (click on the titles to go to the articles):

Looking Ahead: November will be a slightly better month for dividends and my savings rate should remain stable. As noted above, I am expecting a few dividend increases to be announced, which is exciting. Given that I depleted my cash in October, the new capital from savings will enable me to make just one purchase this month, although I have not yet made up my mind about what I am going to buy.

Dividends: I received a total of $124.52 in dividends from the following stocks:

- CNI: $6.47

- GPC: $24.75

- ITW: $15.20

- KO: $15.30

- MDT: $14.30

- PM: $42.50

- UNP: $6.00

Dividend Increases: I was pleased to see a dividend increase announced for one of my stocks (click on the stock to see my post about the increase):

- KMI: 2.9% increase, $1.60 more in annual dividend income

Savings: This month I saved $1,662 (55.9%) of my net income, which is almost identical to what I saved in September and results in year-to-date savings of $14,310.

Transactions: I bought three stocks this month (click on the transactions to see my posts about them): It was one of my busiest months for purchases this year. KMI and CMI are new positions that increase my portfolio's exposure to the energy and industrial sectors, respectively. My purchase of INTC increases the position I started in September. These purchases will increase my annual dividend income by $132.60. I did not sell any stocks for the 10th consecutive month.

Portfolio: My portfolio currently consists of 25 stocks and has a market value of $61,285.58 (including cash), which is a 1.4% increase over last month's value. The increase reflects gains from new capital and dividends being partially offset by capital losses on some existing positions.

Seeking Alpha: I published two new articles on the investing website Seeking Alpha (click on the titles to go to the articles):

- Examining Another Dividend-Growth Large-Cap Fallacy

- Dividend Growth Analysis: Rate Versus Length Of Streak

Looking Ahead: November will be a slightly better month for dividends and my savings rate should remain stable. As noted above, I am expecting a few dividend increases to be announced, which is exciting. Given that I depleted my cash in October, the new capital from savings will enable me to make just one purchase this month, although I have not yet made up my mind about what I am going to buy.

Sunday, October 21, 2012

Book Review: Markets Never Forget (But People Do)

Markets Never Forget (But People Do) (2011) by Ken Fisher

This book can be considered a sequel to the author's previous book, Debunkery, which I read and reviewed earlier this year. The main thesis of this book is that people tend to forget about (or ignore) market history, which results in misconceptions and improbable projections about the relationship between market performance and various economic and political factors. To give some examples from the book:

Note: I read this book in September 2012.

This book can be considered a sequel to the author's previous book, Debunkery, which I read and reviewed earlier this year. The main thesis of this book is that people tend to forget about (or ignore) market history, which results in misconceptions and improbable projections about the relationship between market performance and various economic and political factors. To give some examples from the book:

- In the past few years there has been plenty of talk about the risk of a "double-dip recession," even though it is an improbable event, reflecting less than 10% of past recessions.

- People tend to forget that major drops in the market are often followed soon after by strong rebounds, producing a V-shaped pattern.

- Even though the market's average annual return has been around 10%, it is actually rare for the return in a given year to be around 10%.

- If you are a perma-bear, then you will be wrong more often than right because the market has positive annual returns about two-thirds of the time.

Note: I read this book in September 2012.

Saturday, October 20, 2012

Revisiting Black Monday After 25 Years

Yesterday marked the 25th anniversary of Black Monday (October 19, 1987), when world stock markets plunged and the Dow Jones Industrial Average fell by 22% in a single day. Nightly Business Report has posted the video of that night's broadcast on their website. It provides a fascinating historical look at what happened that day and how people reacted.

Wednesday, October 17, 2012

Dividend Increase: KMI

Kinder Morgan, Inc. (KMI) is increasing its quarterly dividend by 2.9%, from $0.35 to $0.36 per share. Its dividend has been increased every quarter in 2012, resulting in an overall increase of 20% compared with the last quarter of 2011. Given that I own 40 shares of KMI, my quarterly dividend increases from $14.00 to $14.40, which will add an extra $1.60 to my annual dividend income. This dividend increase also boosts my yield on cost to 4.11%. Thus far this year, there have been dividend increases for 23 of the 25 dividend growth stocks in my portfolio.

Dividend News: ABT

There has been some uncertainty about what will happen to the dividend of Abbott Laboratories (ABT) once the company splits at the end of this year. Some clarification was provided on today's earnings call:

The dividend has always been an important component of Abbott's investment identity. We had previously indicated that we expected to combine dividend of the 2 companies to be at least equal to Abbott's pre-separation annual dividend. And we expect AbbVie to be even more focused on shareholder returns in the pharma dividends, paying a larger portion of the dividend.Assuming those dividend rates are approved, the combined dividend increase will be 5.9%, which is rather modest, but it will come a quarter earlier than usual. Note that AbbVie will trade under the ticker ABBV.

With this in mind, today, we're announcing that we expect AbbVie to pay an annual dividend of $1.60 per share, starting with the quarterly dividend to be paid in February. This, like all dividends, will be subject to approval by the future AbbVie board in January 2013. We're also announcing that we expect the new Abbott dividend to be $0.56 per share, in line with its peer group and growth prospects, again, starting with the dividend to be paid in February and again, subject to approval by the Abbott board.

In the end, this combined annual dividend rate of $2.16 for the 2 companies exceeds the current annual dividend rate of $2.04. And this increase is expected to be implemented one quarter earlier than in past years.

Tuesday, October 16, 2012

Dividend Growth Analysis: Rate Versus Length Of Streak

A new article of mine has been published on the investing website Seeking Alpha. The article is entitled Dividend Growth Analysis: Rate Versus Length Of Streak and it looks at the relationship between dividend growth rate and length of the dividend growth streak.

Thursday, October 11, 2012

Stock Bought: INTC

Today I bought shares of Intel (INTC), the world's largest semiconductor chip maker. I wrote about INTC last month when I started a position in the stock. Its price has continued to trend down over the past few weeks, making the stock even more undervalued than before. The company reports its quarterly earnings on October 16, but I do not like to guess how the market will react to earnings, so I deemed it best to take advantage of the buying opportunity already in front of me.

I bought 50 shares of INTC at the price of $21.70 per share, giving me a total of 115 shares at an average price of exactly $22.22 per share (some nice symmetry there) and a 4.03% yield on cost. At the current dividend rate, I can expect to receive quarterly dividends of $25.88, which is $11.25 more than before this purchase. INTC will now contribute a total of $103.52 to my annual dividend income, an increase of $45.00.

My three purchases this week used up all my cash, so I will be waiting on the sidelines until I have new capital at the start of November. On the one hand, this means I will not be able to take advantage of any dips due to earnings that "miss" analyst estimates in the coming weeks. On the other hand, desirable dips might not happen (such was the case in July) and the opportunities that resulted in my recent purchases might be gone by the end of the month. I am continuing to teach myself that it is better to capitalize on good opportunities when they are present than to speculate about future opportunities that may not come to fruition.

I bought 50 shares of INTC at the price of $21.70 per share, giving me a total of 115 shares at an average price of exactly $22.22 per share (some nice symmetry there) and a 4.03% yield on cost. At the current dividend rate, I can expect to receive quarterly dividends of $25.88, which is $11.25 more than before this purchase. INTC will now contribute a total of $103.52 to my annual dividend income, an increase of $45.00.

My three purchases this week used up all my cash, so I will be waiting on the sidelines until I have new capital at the start of November. On the one hand, this means I will not be able to take advantage of any dips due to earnings that "miss" analyst estimates in the coming weeks. On the other hand, desirable dips might not happen (such was the case in July) and the opportunities that resulted in my recent purchases might be gone by the end of the month. I am continuing to teach myself that it is better to capitalize on good opportunities when they are present than to speculate about future opportunities that may not come to fruition.

Wednesday, October 10, 2012

Stock Bought: CMI

For my second purchase today I bought shares of Cummins (CMI), a world leader in the design and manufacture of diesel and natural gas engines. The company is at the forefront of developing better engine technology that meets stricter emission standards and is poised to take advantage of the increasing use of natural gas as a fuel source for vehicles.

I recently posted a quantitative comparison of CMI with one of its competitors in the heavy machinery industry, arguing that it is undervalued despite having solid fundamentals. Here is a recap:

I bought 15 shares of CMI at the price of $88.00 per share, giving me a 2.26% yield on cost. At the current dividend rate, I can expect to receive quarterly dividends of $7.50, which will add a total of $30.00 to my annual dividend income. Cummins is now the 25th stock in my portfolio. I had been waiting for an opportunity to initiate a position in CMI below $90, so I was glad to get it today. The company reports its quarterly earnings on October 30, which could lead to more price action at the end of the month. If the stock is still trading around the current level in early November (when I will have new capital), then I would consider increasing my position.

I recently posted a quantitative comparison of CMI with one of its competitors in the heavy machinery industry, arguing that it is undervalued despite having solid fundamentals. Here is a recap:

- Its 5-year historic growth rates for revenue and earnings are 9.70% and 21.87%, respectively, with low double-digit earnings growth expected over the next few years.

- The company has a great balance sheet, with debt/capital of 9.60%, debt/equity of 12.34%, a current ratio over 2, and ample interest coverage.

- The company has increased its dividend for 7 consecutive years, with an impressive 5-year dividend growth rate of 32.10% and a payout ratio of just 20%. This year's dividend increase was 25%.

- CMI has a P/E of 8.74 (its 5-year average P/E is 15.10), P/S of 0.91, and PEG of 0.76. Using a Dividend Discount Model with a below-average dividend growth rate of 10% and a discount rate of 12%, I calculate a fair value of $110 per share, which implies a 20% margin of safety at the current stock price.

I bought 15 shares of CMI at the price of $88.00 per share, giving me a 2.26% yield on cost. At the current dividend rate, I can expect to receive quarterly dividends of $7.50, which will add a total of $30.00 to my annual dividend income. Cummins is now the 25th stock in my portfolio. I had been waiting for an opportunity to initiate a position in CMI below $90, so I was glad to get it today. The company reports its quarterly earnings on October 30, which could lead to more price action at the end of the month. If the stock is still trading around the current level in early November (when I will have new capital), then I would consider increasing my position.

Stock Bought: KMI

For my first purchase today I bought shares of Kinder Morgan (KMI), the third-largest energy company in North America. The company operates an extensive network of pipelines for transporting natural gas, crude oil, and petroleum products. Its business model is similar to a toll road in that the company collects volume-based fees for transporting raw materials, with limited exposure to the fluctuating prices of those commodities. This results in stable and growing cash flows as energy needs increase over time, and the company's massive asset footprint will likely help it dominate the midstream energy industry for many years to come.

The Kinder Morgan group of companies has an interesting corporate structure. The General Partner (GP) is Kinder Morgan, Inc. (KMI), which pays dividends based on distributions it receives from two Limited Partners (LPs). The first LP is Kinder Morgan Energy Partners, which is represented by two entities that differ only in that KMP gives cash distributions (similar to dividends) and KMR gives share dividends. The second LP is the recently acquired El Paso Pipeline Partners, which is represented by a single entity, EPB, that gives cash distributions. KMP and EPB are examples of Master Limited Partnerships (MLPs), which often have high yields but come with some tax complications. KMI is a C-corporation that provides a way of investing in MLPs without the extra tax issues. Moreover, because of its Incentive Distribution Rights as GP, KMI should be capable of greater dividend growth over time than the LPs.

KMI became a publicly traded stock in early 2011, so it does not have much of a dividend history at this point. However, the company has increased its dividend in 4 of the past 5 quarters and management has expressed a commitment to dividend growth. In fact, management is targeting a dividend growth rate of at least 10% for the next several years, which is not unrealistic given the 14% distribution growth rate for KMP over the past 16 years. In addition, Richard Kinder (the CEO) and other management own about 28% of KMI stock, so it is in their interest to maintain a solid dividend.

It is difficult to come up with a valuation for KMI because of the unique characteristics of the MLPs for which it is the GP. In addition, its balance sheet is difficult to assess because the company still has to "drop down" assets from its purchase of El Paso Pipeline Partners. However, using a Dividend Discount Model with a dividend growth rate of 10% (matching their target) and a discount rate of 14%, I calculate a fair value of $38.50 per share, which is slightly above the current stock price.

I bought 40 shares of KMI at the price of $34.85 per share, giving me a 4.00% yield on cost. (I set my limit price with the goal of getting that YOC.) At the current dividend rate, I can expect to receive quarterly dividends of $14.00, which will add a total of $56.00 to my annual dividend income. The stock will go ex-dividend later this month, so I will receive my first dividend payment in November. Kinder Morgan is now the 24th stock in my portfolio, adding some nice diversification in the energy sector.

The Kinder Morgan group of companies has an interesting corporate structure. The General Partner (GP) is Kinder Morgan, Inc. (KMI), which pays dividends based on distributions it receives from two Limited Partners (LPs). The first LP is Kinder Morgan Energy Partners, which is represented by two entities that differ only in that KMP gives cash distributions (similar to dividends) and KMR gives share dividends. The second LP is the recently acquired El Paso Pipeline Partners, which is represented by a single entity, EPB, that gives cash distributions. KMP and EPB are examples of Master Limited Partnerships (MLPs), which often have high yields but come with some tax complications. KMI is a C-corporation that provides a way of investing in MLPs without the extra tax issues. Moreover, because of its Incentive Distribution Rights as GP, KMI should be capable of greater dividend growth over time than the LPs.

KMI became a publicly traded stock in early 2011, so it does not have much of a dividend history at this point. However, the company has increased its dividend in 4 of the past 5 quarters and management has expressed a commitment to dividend growth. In fact, management is targeting a dividend growth rate of at least 10% for the next several years, which is not unrealistic given the 14% distribution growth rate for KMP over the past 16 years. In addition, Richard Kinder (the CEO) and other management own about 28% of KMI stock, so it is in their interest to maintain a solid dividend.

It is difficult to come up with a valuation for KMI because of the unique characteristics of the MLPs for which it is the GP. In addition, its balance sheet is difficult to assess because the company still has to "drop down" assets from its purchase of El Paso Pipeline Partners. However, using a Dividend Discount Model with a dividend growth rate of 10% (matching their target) and a discount rate of 14%, I calculate a fair value of $38.50 per share, which is slightly above the current stock price.

I bought 40 shares of KMI at the price of $34.85 per share, giving me a 4.00% yield on cost. (I set my limit price with the goal of getting that YOC.) At the current dividend rate, I can expect to receive quarterly dividends of $14.00, which will add a total of $56.00 to my annual dividend income. The stock will go ex-dividend later this month, so I will receive my first dividend payment in November. Kinder Morgan is now the 24th stock in my portfolio, adding some nice diversification in the energy sector.

Friday, October 5, 2012

Examining Another Dividend-Growth Large-Cap Fallacy

A new article of mine has been published on the investing website Seeking Alpha. The article is entitled Examining Another Dividend-Growth Large-Cap Fallacy and it looks at the relationship between market capitalization and dividend growth rate among dividend growth stocks.

Tuesday, October 2, 2012

Stock Thoughts: CMI vs. CAT

In my ongoing quest to find undervalued dividend growth stocks I have focused recently on two industrial companies that manufacture and distribute heavy machinery: Cummins (CMI) and Caterpillar (CAT). Cummins designs and produces diesel and natural gas engines, as well as various engine-related components. Caterpillar also builds engines, but it has a more diverse product array that includes construction/mining machines and industrial gas turbines.

The purpose of this post is to organize, compare, and share some of the quantitative information I have compiled on the two companies. It is intended to be a quick, side-by-side numerical snapshot rather than a comprehensive analysis. I will start with some stock price information (as of October 2):

Both stocks are trading more than 25% below their 52-week highs, suggesting they have fallen out of favor recently. This becomes more evident upon examination of various price ratios:

Both stocks are trading more than 25% below their 52-week highs, suggesting they have fallen out of favor recently. This becomes more evident upon examination of various price ratios:

The current P/E, P/S, and P/B ratios are below their 5-year averages, indicating that both stocks are undervalued. It seems as though the market has historically given a higher valuation to CAT than to CMI. This observation, coupled with the PEG ratios and various fair value estimates I have seen, suggests that CAT might be slightly more undervalued than CMI. The next table shows recent growth rates:

The current P/E, P/S, and P/B ratios are below their 5-year averages, indicating that both stocks are undervalued. It seems as though the market has historically given a higher valuation to CAT than to CMI. This observation, coupled with the PEG ratios and various fair value estimates I have seen, suggests that CAT might be slightly more undervalued than CMI. The next table shows recent growth rates:

Here we see that CMI has had superior revenue and earnings growth in recent years, but CAT is expected to have higher growth going forward (which is a reason for its lower PEG ratio). However, it is notoriously difficult to accurately predict future growth, so I consider the projections to be in the same ballpark for both companies. Next are some measures of management effectiveness:

Here we see that CMI has had superior revenue and earnings growth in recent years, but CAT is expected to have higher growth going forward (which is a reason for its lower PEG ratio). However, it is notoriously difficult to accurately predict future growth, so I consider the projections to be in the same ballpark for both companies. Next are some measures of management effectiveness:

ROA and ROE are acceptable for both companies. The comparison becomes more interesting when you look at some balance sheet details:

ROA and ROE are acceptable for both companies. The comparison becomes more interesting when you look at some balance sheet details:

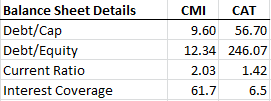

CMI has a strong balance sheet with low debt, a high current ratio, and excellent interest coverage. In contrast, CAT has a mediocre balance sheet with a considerable amount of debt. Given that these companies operate in a cyclical industry, I place great weight on the balance sheet. As a dividend growth investor, I also give a lot of weight to the dividend:

CMI has a strong balance sheet with low debt, a high current ratio, and excellent interest coverage. In contrast, CAT has a mediocre balance sheet with a considerable amount of debt. Given that these companies operate in a cyclical industry, I place great weight on the balance sheet. As a dividend growth investor, I also give a lot of weight to the dividend:

The yields and payout ratios are similar, but CMI has had much stronger dividend growth in recent years, although CAT has a much longer dividend growth streak. I find myself more impressed by the recent dividend growth from CMI.

The yields and payout ratios are similar, but CMI has had much stronger dividend growth in recent years, although CAT has a much longer dividend growth streak. I find myself more impressed by the recent dividend growth from CMI.

Summary and Conclusions: This purely quantitative comparison shows that CMI and CAT are similar in many respects, the main one being that both stocks are undervalued. Using a Dividend Discount Model with a 10% dividend growth rate and 12% discount rate, I get a fair value of $110 for CMI and $114 for CAT. These values imply there is a margin of safety of at least 15% at current prices.

Even though I did not show any historical trend data, both companies recovered quickly from the recession and seem to be doing well. However, CAT recently lowered its guidance out to 2015, which may hint at some future earnings instability (CMI reduced its short-term guidance earlier this year). Despite near-term economic pressures, I think both companies would represent suitable long-term investments, especially when worldwide economic growth picks up.

That said, if I were to choose just one of them as an investment, then I would probably go with CMI. From a quantitative perspective, I like its strong balance sheet and recent dividend growth. From a qualitative perspective, I like the company's leadership in developing better engine technology that meets stricter emission standards. The increasing use of natural gas as a fuel source should also benefit the company. For these reasons, I am considering CMI as a potential addition to my portfolio.

The purpose of this post is to organize, compare, and share some of the quantitative information I have compiled on the two companies. It is intended to be a quick, side-by-side numerical snapshot rather than a comprehensive analysis. I will start with some stock price information (as of October 2):

Summary and Conclusions: This purely quantitative comparison shows that CMI and CAT are similar in many respects, the main one being that both stocks are undervalued. Using a Dividend Discount Model with a 10% dividend growth rate and 12% discount rate, I get a fair value of $110 for CMI and $114 for CAT. These values imply there is a margin of safety of at least 15% at current prices.

Even though I did not show any historical trend data, both companies recovered quickly from the recession and seem to be doing well. However, CAT recently lowered its guidance out to 2015, which may hint at some future earnings instability (CMI reduced its short-term guidance earlier this year). Despite near-term economic pressures, I think both companies would represent suitable long-term investments, especially when worldwide economic growth picks up.

That said, if I were to choose just one of them as an investment, then I would probably go with CMI. From a quantitative perspective, I like its strong balance sheet and recent dividend growth. From a qualitative perspective, I like the company's leadership in developing better engine technology that meets stricter emission standards. The increasing use of natural gas as a fuel source should also benefit the company. For these reasons, I am considering CMI as a potential addition to my portfolio.

Monthly Review: September 2012

Here is a review of what happened in September:

Dividends: I received a total of $134.48 in dividends from the following stocks:

Dividend Increases: I was pleased to see dividend increases announced for two of my stocks (click on each stock to see my post about the increase): These are my two largest dividend payers, so I am happy to get double-digit percent increases. Thus far this year, there have been dividend increases for 20 of the 23 dividend growth stocks in my portfolio. I expect increases for the remaining three stocks (ADM, BDX, and UNP) to be announced in November.

Savings: This month I saved $1,668 (56.1%) of my net income, which results in year-to-date savings of $12,648. I achieved my goal of $12,000 in savings for 2012! When I set the goal at the start of the year, I did not have a reliable estimate of how much I could save each month. It feels great to know that I was able to save more than I anticipated. I am curious to see how much my total savings will be at the end of the year.

Transactions: I bought two stocks this month (click on the transactions to see my posts about them): As discussed in my posts, I consider these to be good purchases from a valuation standpoint. The first purchase increases my position in NSC, making the railroad stock the third-largest position in my portfolio. The second purchase is my first new position in several months and I think a high-quality technology stock such as INTC adds some nice diversification to my portfolio. These purchases will increase my annual dividend income by $98.52. I did not sell any stocks for the 9th consecutive month.

Portfolio: My portfolio currently consists of 23 stocks and has a market value of $60,437.16 (including cash), which is a 2.4% increase over last month's value. About 72% of the increase came from new capital and the rest was due to capital gains and dividends.

Seeking Alpha: I published one new article on the investing website Seeking Alpha (click on the title to go to the article): Curiously, this turned out to be my least popular article in terms of page views, even though it seemed to get a good reception in the comment section. Oh well! In September I earned a total of $44.37 from this article and additional page views of my previous articles. My Q3 total is $235.66 (which will be paid in October) and my year-to-date total is $579.60.

Looking Ahead: October will be a decent month for dividends, only slightly less than what I received in September. My savings rate should be good. My two recent purchases used up a modest amount of cash, but once I add the new capital from my September savings, I will have enough cash to make two purchases. A lot of earnings will be reported in the second half of October, so I am tempted to wait and see which stocks dip on "disappointing" earnings. However, if a good opportunity comes up between now and then, I might take advantage of it.

Dividends: I received a total of $134.48 in dividends from the following stocks:

- ADM: $10.50

- BDX: $11.25

- CVX: $18.00

- JNJ: $21.35

- MCD: $35.00

- NSC: $25.00

- UTX: $13.38

Dividend Increases: I was pleased to see dividend increases announced for two of my stocks (click on each stock to see my post about the increase): These are my two largest dividend payers, so I am happy to get double-digit percent increases. Thus far this year, there have been dividend increases for 20 of the 23 dividend growth stocks in my portfolio. I expect increases for the remaining three stocks (ADM, BDX, and UNP) to be announced in November.

Savings: This month I saved $1,668 (56.1%) of my net income, which results in year-to-date savings of $12,648. I achieved my goal of $12,000 in savings for 2012! When I set the goal at the start of the year, I did not have a reliable estimate of how much I could save each month. It feels great to know that I was able to save more than I anticipated. I am curious to see how much my total savings will be at the end of the year.

Transactions: I bought two stocks this month (click on the transactions to see my posts about them): As discussed in my posts, I consider these to be good purchases from a valuation standpoint. The first purchase increases my position in NSC, making the railroad stock the third-largest position in my portfolio. The second purchase is my first new position in several months and I think a high-quality technology stock such as INTC adds some nice diversification to my portfolio. These purchases will increase my annual dividend income by $98.52. I did not sell any stocks for the 9th consecutive month.

Portfolio: My portfolio currently consists of 23 stocks and has a market value of $60,437.16 (including cash), which is a 2.4% increase over last month's value. About 72% of the increase came from new capital and the rest was due to capital gains and dividends.

Seeking Alpha: I published one new article on the investing website Seeking Alpha (click on the title to go to the article): Curiously, this turned out to be my least popular article in terms of page views, even though it seemed to get a good reception in the comment section. Oh well! In September I earned a total of $44.37 from this article and additional page views of my previous articles. My Q3 total is $235.66 (which will be paid in October) and my year-to-date total is $579.60.

Looking Ahead: October will be a decent month for dividends, only slightly less than what I received in September. My savings rate should be good. My two recent purchases used up a modest amount of cash, but once I add the new capital from my September savings, I will have enough cash to make two purchases. A lot of earnings will be reported in the second half of October, so I am tempted to wait and see which stocks dip on "disappointing" earnings. However, if a good opportunity comes up between now and then, I might take advantage of it.

Monday, September 24, 2012

Stock Bought: INTC

Today I bought shares of Intel (INTC), the world's largest semiconductor chip maker. The company dominates the market for microprocessors in personal computers (PCs) and continues to be a leader in technological product development.

Intel has produced solid operating results in recent years, with 5-year growth rates of 8.8% for revenue and 22.7% for earnings, high margins, strong cash flows, and good returns on equity. The company's financial position is excellent, with $13.7B in cash, $7.2B in debt, debt/capital of 13.4%, debt/equity of 14.8%, 189x interest coverage, and a current ratio of 2.4. It has an A+ credit rating from S&P and a safety rating of 1 from Value Line.

For a tech company, Intel has a pretty good dividend history. The company has increased its dividend for 9 consecutive years and has a 5-year dividend growth rate of 14.4%. The most recent dividend increase was 7.1%, announced in May. The payout ratio is a modest 38%.

Regarding valuation, I consider Intel to be undervalued with a P/E of 9.6 (its 5-year average P/E is 17.1), P/S of 2.1, and PEG of 0.9. Using a Dividend Discount Model with a below-average dividend growth rate of 9% and a discount rate of 12%, I calculate a fair value over $32 per share, which I think is a reasonable estimate.

Intel's stock price has been beaten down in recent months, reaching a 10-month low today. The stock is trading 20% below its 52-week high set in early May. The drop in stock price reflects the perception that PC sales are on the decline and the recognition that Intel has yet to gain much market share in mobile devices. In addition, earlier this month the company lowered its quarterly revenue outlook. I think the fears about PCs being replaced by tablets and smart phones are overblown. There are many workplaces (such as my own) that will likely continue using PCs for many years, in part because they are much more powerful than mobile devices. I also think the concerns about Intel's lack of presence in the mobile market are overdone. To put a positive spin on it, given that the company has yet to gain much market share in the area, there is plenty of room for future growth. Intel invests heavily in R&D and has top-notch fabrication facilities, so I think it is only a matter of time before they make significant inroads in the mobile market.

I bought 65 shares of INTC at the price of $22.62 per share, giving me a 3.96% yield on cost. At the current dividend rate, I can expect to receive quarterly dividends of $14.63, which will add a total of $58.52 to my annual dividend income. Intel is now the 23rd stock in my portfolio and my first new position since April. Even though I am wary of the technology sector in general, Intel is a solid, profitable company that I feel comfortable having in my portfolio. For that reason, I would consider increasing my position on a further decline in the stock price.

I am pleased that I was able to find a second great opportunity to deploy cash this month (the first being my purchase of NSC last week). I think I am getting better at appreciating that it is a "market of stocks" rather than a stock market, so regardless of what the broader market is doing, it is best to stay focused on finding individual dividend growth stocks that are available at attractive valuations.

Intel has produced solid operating results in recent years, with 5-year growth rates of 8.8% for revenue and 22.7% for earnings, high margins, strong cash flows, and good returns on equity. The company's financial position is excellent, with $13.7B in cash, $7.2B in debt, debt/capital of 13.4%, debt/equity of 14.8%, 189x interest coverage, and a current ratio of 2.4. It has an A+ credit rating from S&P and a safety rating of 1 from Value Line.

For a tech company, Intel has a pretty good dividend history. The company has increased its dividend for 9 consecutive years and has a 5-year dividend growth rate of 14.4%. The most recent dividend increase was 7.1%, announced in May. The payout ratio is a modest 38%.

Regarding valuation, I consider Intel to be undervalued with a P/E of 9.6 (its 5-year average P/E is 17.1), P/S of 2.1, and PEG of 0.9. Using a Dividend Discount Model with a below-average dividend growth rate of 9% and a discount rate of 12%, I calculate a fair value over $32 per share, which I think is a reasonable estimate.

Intel's stock price has been beaten down in recent months, reaching a 10-month low today. The stock is trading 20% below its 52-week high set in early May. The drop in stock price reflects the perception that PC sales are on the decline and the recognition that Intel has yet to gain much market share in mobile devices. In addition, earlier this month the company lowered its quarterly revenue outlook. I think the fears about PCs being replaced by tablets and smart phones are overblown. There are many workplaces (such as my own) that will likely continue using PCs for many years, in part because they are much more powerful than mobile devices. I also think the concerns about Intel's lack of presence in the mobile market are overdone. To put a positive spin on it, given that the company has yet to gain much market share in the area, there is plenty of room for future growth. Intel invests heavily in R&D and has top-notch fabrication facilities, so I think it is only a matter of time before they make significant inroads in the mobile market.

I bought 65 shares of INTC at the price of $22.62 per share, giving me a 3.96% yield on cost. At the current dividend rate, I can expect to receive quarterly dividends of $14.63, which will add a total of $58.52 to my annual dividend income. Intel is now the 23rd stock in my portfolio and my first new position since April. Even though I am wary of the technology sector in general, Intel is a solid, profitable company that I feel comfortable having in my portfolio. For that reason, I would consider increasing my position on a further decline in the stock price.

I am pleased that I was able to find a second great opportunity to deploy cash this month (the first being my purchase of NSC last week). I think I am getting better at appreciating that it is a "market of stocks" rather than a stock market, so regardless of what the broader market is doing, it is best to stay focused on finding individual dividend growth stocks that are available at attractive valuations.

Thursday, September 20, 2012

Dividend Increase: MCD

McDonald's (MCD) is increasing its quarterly dividend by 10.0%, from $0.70 to $0.77 per share, putting the company on track for its 36th consecutive year of dividend growth. Given that I own 50 shares of MCD, my quarterly dividend increases from $35.00 to $38.50, which will add an extra $14.00 to my annual dividend income. This dividend increase also boosts my yield on cost to 3.45%. Thus far this year, there have been dividend increases for 19 of the 22 dividend growth stocks in my portfolio. I'm lovin' it!

On an unrelated note, this is my 100th post since starting this blog. I have found this blog to be great for keeping track of my investments, staying disciplined about my investing strategy, and interacting with like-minded investors. Thank you to everyone who has visited (my total visit count recently passed 20,000) and shared their thoughts about investing!

On an unrelated note, this is my 100th post since starting this blog. I have found this blog to be great for keeping track of my investments, staying disciplined about my investing strategy, and interacting with like-minded investors. Thank you to everyone who has visited (my total visit count recently passed 20,000) and shared their thoughts about investing!

Stock Bought: NSC

Today I bought shares of Norfolk Southern (NSC), a major North American railroad company. This is the third time I have added to my position in NSC this year, with previous purchases occurring in January and March.

NSC dropped over 9% today after the company lowered its Q3 earnings outlook (other railroad stocks also fell on the news). Continued declines in coal and merchandise shipments are expected to reduce revenues, although these effects will be partially offset by growth in intermodal volumes. While this news is disappointing, I consider it to be a short-term problem that will not dampen the company's long-term growth prospects. Coal volumes have been lower this year due to unusually warm winter weather, but this trend will likely flatten out or reverse once we return to more normal winter temperatures.

Despite the warning about earnings, I think management continues to have a positive view of the company's future. A strong indicator is the fact that NSC has increased its dividend twice this year, by 9.3% in January and by 6.4% in August. Note that the August dividend increase occurred after coal volumes had already been declining for several months. I think the company has responsible management and they would not grow the dividend in this manner if they were worried about future earnings.

From a valuation standpoint, I consider NSC to be undervalued with a P/E of 11.3 (its historic P/E is about 14.4), P/S of 1.9, and PEG of 0.88. Even if one were to lower future earnings expectations, the PEG would still likely be near 1. Today's drop in stock price pushed NSC over the 3% yield point ($66.67) and if you look at its historic yield over the past 10 years, it rarely stays above 3% for a long time. Using a Dividend Discount Model with a projected dividend growth rate of only 8% (which is well below historic averages) and a discount rate of 11%, I calculate a fair value of $72 for NSC, which I think is an extremely conservative estimate.

I bought 20 shares of NSC at the price of $65.98 per share, giving me a total of 70 shares at an average price of $70.25 per share and a 2.83% yield on cost. Note that I was able to average down from my previous cost basis of $71.96. At the current dividend rate, I can expect to receive quarterly dividends from NSC of $35.00, which is $10.00 more than what I was getting before this purchase. NSC will now contribute a total of $140.00 to my annual dividend income, which is $40.00 more than before. This purchase makes NSC the second-largest position in my portfolio, slightly behind MCD and slightly ahead of PM in market value.

It was nice to deploy some cash after a summertime lull. With the market near an all-time high, it has been difficult to find undervalued stocks. For that reason, it seemed appropriate to take advantage of the major drop in NSC today to lower my cost basis and increase my ownership of a great company. I still have enough cash on hand to make two more purchases, so hopefully Mr. Market gives me more good buying opportunities.

NSC dropped over 9% today after the company lowered its Q3 earnings outlook (other railroad stocks also fell on the news). Continued declines in coal and merchandise shipments are expected to reduce revenues, although these effects will be partially offset by growth in intermodal volumes. While this news is disappointing, I consider it to be a short-term problem that will not dampen the company's long-term growth prospects. Coal volumes have been lower this year due to unusually warm winter weather, but this trend will likely flatten out or reverse once we return to more normal winter temperatures.